Your savings rate—the share of gross income you keep and invest—is the single number that predicts when work becomes optional. A 20% rate means roughly 37 years to financial independence; push it to 50% and that drops to about 17. This guide gives you the complete formula (including the 401k match and principal paydown most calculators miss), benchmarks at every savings level, and the specific levers I used to reach a $1.6M net worth by 36—so you can calculate your rate in minutes and see exactly what raising it by 5 or 10 points does to your timeline.

Yet most people don't even know what their savings rate is, let alone how to optimize it. After reaching a net worth of $1.6 million by age 36, I can tell you that understanding and maximizing my savings rate was the key driver of that success.

Let me show you how to calculate your true savings rate, interpret what it means for your financial independence timeline, and share the strategies that helped me retire early.

Yet most people don't even know what their savings rate is, let alone how to optimize it. After reaching a net worth of $1.6 million by age 36, I can tell you that understanding and maximizing my savings rate was the key driver of that success.

Let me show you how to calculate your true savings rate, interpret what it means for your financial independence journey, and most importantly, how to increase it systematically. Use our spreadsheet to calculate your savings rate in minutes.

What's Your Emergency Fund Runway?

Calculate how many months of freedom you can afford right now

Example: $30,000 saved ÷ $3,000/month = 10 months of freedom

What Is a Savings Rate (And Why Most People Calculate It Wrong)

Your savings rate is the percentage of your income that you don't spend—money that goes toward building wealth rather than covering current lifestyle costs.

The Standard Formula: Savings Rate = (Income - Expenses) ÷ Income × 100

But here's where most people mess up: They only count money they actively move to savings accounts, ignoring other forms of wealth building.

The Complete Savings Rate Formula

True Savings Rate = (All Wealth Building) ÷ (Gross Income) × 100

All Wealth Building includes:

- 401k contributions (including employer match)

- IRA contributions

- Taxable investment account contributions

- Extra mortgage principal payments

- Money moved to savings accounts

- Emergency fund contributions

- Any other money that increases your net worth

Gross Income includes:

- Salary or wages (pre-tax)

- Bonuses and commissions

- Side hustle income

- Investment dividends and interest

- Any other money coming in

Example Calculation:

- Gross income: $80,000

- 401k contribution: $8,000

- Employer match: $4,000

- IRA contribution: $6,000

- Additional savings: $4,000

- Total wealth building: $22,000

- True savings rate: 27.5%

Many people would only count the $4,000 in "savings" and report a 5% savings rate, missing the full picture of their wealth building.

The Savings Rate Calculator

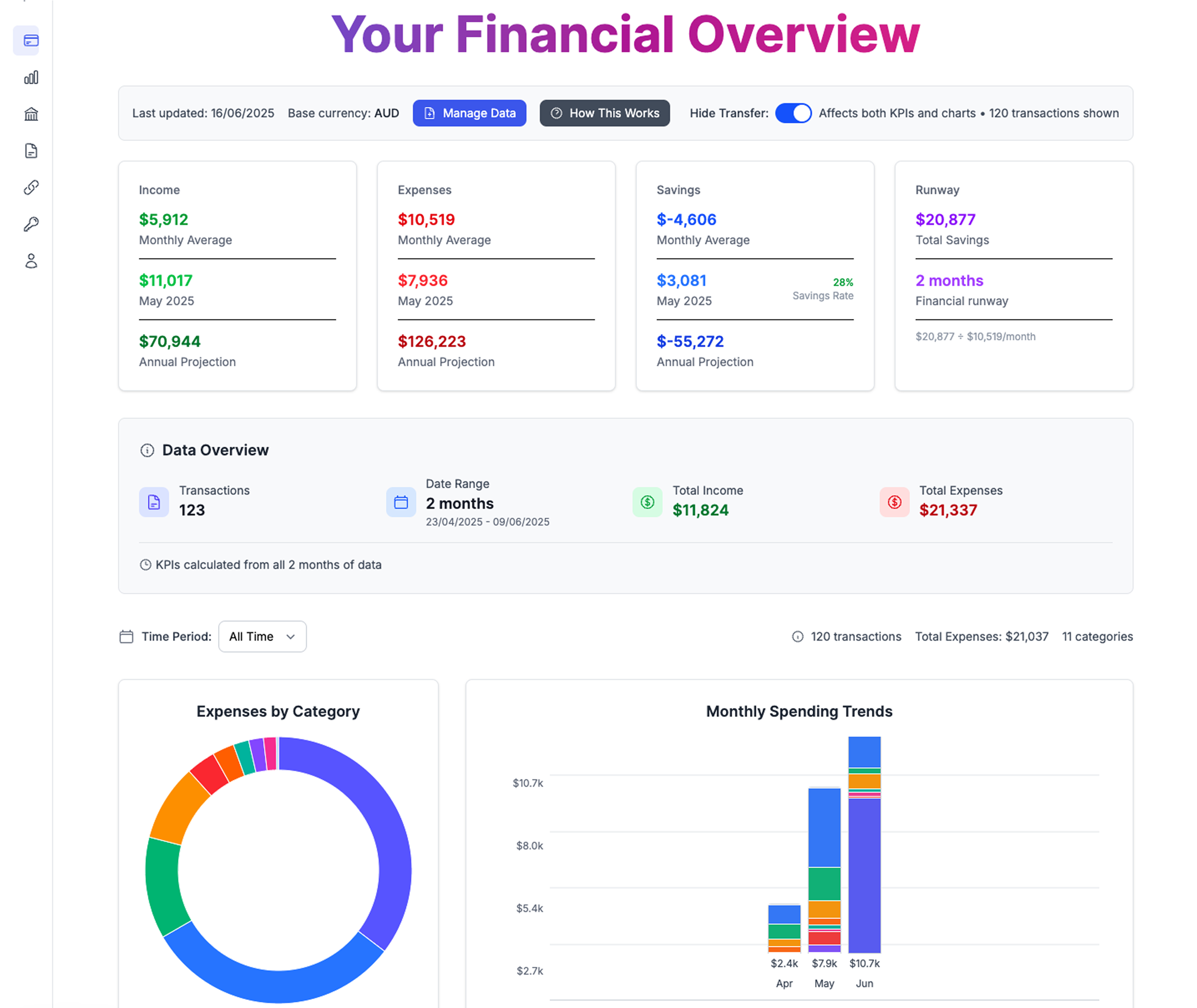

Complete financial overview showing your savings rate, spending patterns, and path to financial independence

Complete financial overview showing your savings rate, spending patterns, and path to financial independence

Want to do this automatically? Our Google Sheet template calculates your true savings rate for you.

Step 1: Calculate Your Monthly Income

Employment Income:

- Monthly gross salary: $______

- Bonuses (monthly average): $______

- Commission (monthly average): $______

- Employer 401k match: $______

Other Income:

- Side hustle income: $______

- Investment dividends/interest: $______

- Rental income (net): $______

- Any other regular income: $______

Total Monthly Income: $______

Step 2: Calculate Your Monthly Wealth Building

Retirement Contributions:

- 401k contribution: $______

- IRA contribution: $______

- Other retirement accounts: $______

Investment Contributions:

- Taxable brokerage accounts: $______

- Index funds: $______

- Individual stocks: $______

Savings Contributions:

- High-yield savings: $______

- Emergency fund: $______

- Goal-specific savings: $______

Debt Reduction (Wealth Building):

- Extra mortgage principal: $______

- Extra payments on good debt: $______

Total Monthly Wealth Building: $______

Step 3: Calculate Your Savings Rate

Monthly Savings Rate = (Monthly Wealth Building ÷ Monthly Income) × 100

Your Monthly Savings Rate: ______%

Interpreting Your Savings Rate

0-10%: Getting Started

- Reality: You're covering basics but not building wealth quickly

- Timeline to FIRE: 40+ years of working

- Priority: Focus on expense reduction and income increases

- Next Goal: Reach 15% as quickly as possible

10-20%: Building Foundation

- Reality: Following conventional financial advice

- Timeline to FIRE: 30-40 years

- Priority: Optimize major expenses and increase earnings

- Next Goal: Push toward 25% for meaningful acceleration

20-30%: Serious Wealth Building

- Reality: Above-average financial discipline

- Timeline to FIRE: 25-35 years

- Priority: Fine-tune optimization and consider income growth

- Next Goal: Reach 30%+ for substantial timeline reduction

30-50%: Accelerated Path

- Reality: Aggressive wealth building with lifestyle optimization

- Timeline to FIRE: 15-25 years

- Priority: Maintain consistency and optimize investments

- Achievement: You're in the top 5% of savers

50%+: FIRE Fast Track

- Reality: Extreme optimization or high income with controlled lifestyle

- Timeline to FIRE: 10-17 years

- Priority: Ensure sustainable lifestyle and tax optimization

- Achievement: You're approaching financial independence rapidly

The FIRE Timeline Calculator

Your savings rate directly determines when you can achieve financial independence. The FIRE movement is built on this core insight: control your savings rate, and you control your timeline.

Years to FIRE by Savings Rate:

- 10% savings rate: 51 years

- 15% savings rate: 43 years

- 20% savings rate: 37 years

- 25% savings rate: 32 years

- 30% savings rate: 28 years

- 40% savings rate: 22 years

- 50% savings rate: 17 years

- 60% savings rate: 12.5 years

- 70% savings rate: 8.5 years

Assumptions: 7% real investment returns, withdrawing 4% annually in retirement

The Math Behind It: These calculations use the formula for financial independence: 25 × Annual Expenses = FIRE Number

If you spend $40,000 annually, you need $1,000,000 to be financially independent at a 4% withdrawal rate. Use our FIRE number calculator to find your exact target based on your specific spending.

Which FIRE Style Matches Your Savings Rate?

Your savings rate naturally aligns with different FIRE approaches:

- Lean FIRE (50%+ savings rate): Minimize lifestyle costs, reach independence faster—often in under 15 years. Lean FIRE calculator →

- Traditional FIRE (30-50% savings rate): Balance lifestyle enjoyment with aggressive saving.

- Fat FIRE (20-35% savings rate): Build enough wealth to maintain a premium lifestyle in retirement. Fat FIRE calculator →

- Coast FIRE (any savings rate): Reach a point where existing investments will compound to your FIRE number without additional contributions—then optional work covers expenses. Coast FIRE calculator →

Savings Rate Across All FIRE Variants: Picking Your Path

Most FIRE guides treat savings rate as a one-size-fits-all number, but your ideal rate depends heavily on which FIRE variant you're targeting. Understanding the full range of FIRE variants helps you pick a realistic, sustainable target rather than chasing someone else's extreme.

| FIRE Variant | Typical Savings Rate | Why |

|---|---|---|

| Lean FIRE | 50–70%+ | Minimalist lifestyle, fastest path |

| Traditional FIRE | 30–50% | Balanced lifestyle + aggressive saving |

| Fat FIRE | 20–35% | High income compensates for higher spending target |

| Coast FIRE | Variable early, lower later | Front-loads savings, then coasts |

| Barista FIRE | 25–40% | Part-time income covers gap expenses |

The Coast FIRE vs. Barista FIRE comparison is especially relevant if you're not sure you want to push for 100% financial independence before reducing work. Both strategies rely on hitting a savings milestone early—then your rate can drop because you're either coasting on compound growth or supplementing with part-time income.

Practical implication: If you're targeting Barista FIRE, a 25–35% savings rate for 10–12 years may be enough to build the portfolio that covers your gap. You don't need to sacrifice your present life to hit a 50%+ rate.

Building a Budget System That Protects Your Savings Rate

The biggest enemy of a high savings rate isn't a major purchase—it's lifestyle creep: dozens of small spending increases that compound over months and years without you noticing. A structured budget system is the most reliable way to prevent this.

A zero-based budget spreadsheet forces every dollar to have a job at the start of each month. By pre-assigning money to savings before allocating it to expenses, you make your savings rate the constraint that everything else must fit around—not an afterthought.

For those tracking irregular or freelance income, the challenge is different: your savings rate will vary month to month. In high-income months, resist the urge to inflate lifestyle—redirect the excess to investments instead. A freelancer budget for irregular income built around income smoothing can help you maintain a consistent effective savings rate even when income swings wildly.

The key budget principle: Design your budget so that savings happen on day one of the month—before you can spend it. This is called paying yourself first, and it's the structural reason high savers consistently outperform average savers with similar incomes.

How I Reached a High Savings Rate (Real Numbers)

Let me share my actual progression to illustrate how savings rates can grow over time:

Years 1-3 (Age 21-24): 15% Savings Rate

- Income: $45,000

- Savings: $6,750/year

- Focus: Building habits, learning basics

Years 4-7 (Age 25-28): 25% Savings Rate

- Income: $65,000

- Savings: $16,250/year

- Changes: Increased 401k, reduced lifestyle inflation

Years 8-12 (Age 29-33): 40% Savings Rate

- Income: $95,000

- Savings: $38,000/year

- Changes: Optimized housing, increased income, automated everything

Years 13-15 (Age 34-36): 55% Savings Rate

- Income: $140,000

- Savings: $77,000/year

- Changes: Peak earning years, controlled lifestyle, focused on FIRE

Key insight: My savings rate increased faster than my income because I treated raises as savings opportunities, not lifestyle upgrades.

Smart suggestions help optimize your spending and identify opportunities to increase your savings rate

Smart suggestions help optimize your spending and identify opportunities to increase your savings rate

Our spreadsheet can help you find these opportunities in your own spending.

Strategies to Increase Your Savings Rate

The Two-Lever Approach

You can increase your savings rate by:

- Reducing expenses (easier to control)

- Increasing income (higher potential impact)

Most people focus entirely on expense reduction, but the highest savings rates come from optimizing both.

Expense Optimization Strategies

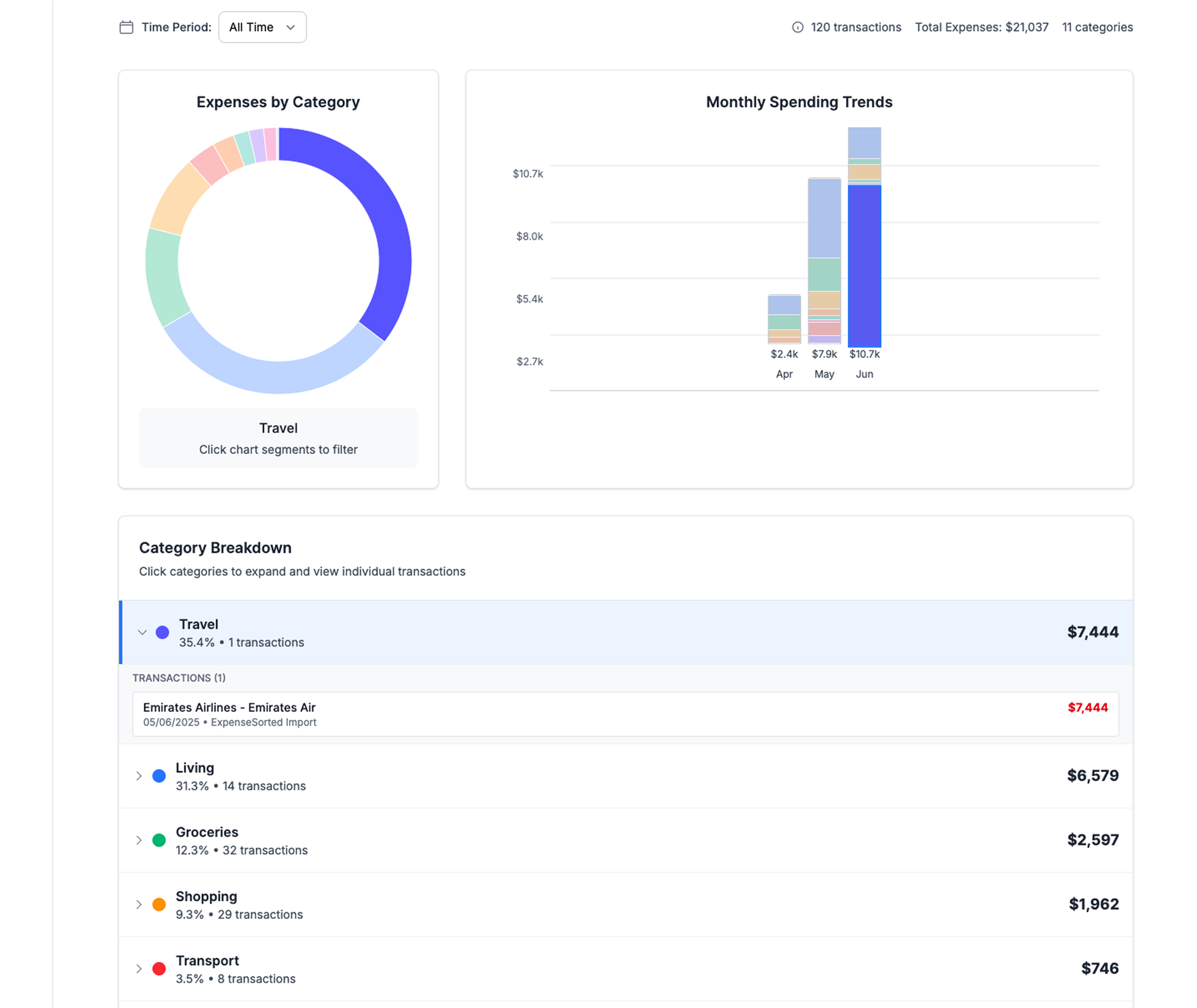

Intelligent expense categorization helps identify the biggest opportunities for increasing your savings rate

Intelligent expense categorization helps identify the biggest opportunities for increasing your savings rate

The Big Three (Focus Here First):

-

Housing (Typically 25-35% of income)

- Consider house hacking (rent out rooms)

- Move to a lower-cost area if possible

- Downsize if you're over-housed

- Refinance or pay extra principal

-

Transportation (Typically 10-20% of income)

- Buy reliable used cars with cash

- Consider one car for couples

- Live closer to work to reduce commuting costs

- Use public transportation where viable

-

Food (Typically 10-15% of income)

- Cook at home more frequently

- Meal plan to reduce waste

- Focus on cost-effective, healthy staples

- Limit restaurant spending to social occasions

The Smaller Wins:

- Cancel unused subscriptions

- Negotiate insurance rates annually

- Optimize utilities and phone plans

- Reduce discretionary shopping

Hidden Savings Rate Killers — Irregular Expenses:

One underrated drag on savings rates is irregular but predictable expenses: car repairs, home maintenance, holiday gifts, annual insurance premiums. Most people treat these as emergencies, which forces them to raid savings or go into debt—both of which destroy the effective savings rate.

The fix is sinking funds: dedicated sub-accounts for each predictable irregular expense. By setting aside $100/month for car maintenance, you never face a $1,200 "unexpected" bill. Your savings rate stays intact because you planned for the outflow in advance.

Income Optimization Strategies

Career Development:

- Negotiate salary increases annually

- Develop high-value skills

- Change jobs strategically for 10-20% raises

- Pursue promotions aggressively

Side Income:

- Freelance or consult in your expertise area

- Start a side business

- Rent out assets (car, tools, space)

- Create passive income streams

Investment Income:

- Focus on dividend-growing investments

- Real estate investment (REITs or direct)

- Build income-producing assets

Advanced Savings Rate Optimization

Tax-Advantaged Account Prioritization

Order of Operations:

- 401k up to employer match (free money)

- High-yield savings for emergency fund

- IRA contribution (traditional or Roth)

- Max out 401k ($23,000 in 2024)

- Taxable investment accounts

- Additional tax-advantaged accounts (HSA, etc.)

Geographic Arbitrage

Your savings rate can increase dramatically by optimizing your location:

- High income, low cost area: Maximum savings potential

- Remote work: Access high-paying jobs from low-cost areas

- International arbitrage: Earn US wages, live in lower-cost countries

The Automation Strategy

High savings rates require automation:

- Direct deposit split: Send savings directly to investment accounts

- Automatic investments: Dollar-cost average into index funds

- Automatic bill pay: Reduce decision fatigue on fixed expenses

- Savings rate increases: Automatically increase contributions with raises

Seamless bank data import ensures your savings rate calculations stay accurate with minimal effort

Seamless bank data import ensures your savings rate calculations stay accurate with minimal effort

Common Savings Rate Mistakes

Mistake 1: Focusing on Percentages Too Early

If your income is very low, focus on increasing income before optimizing percentages. A 50% savings rate on $30,000 income builds wealth slower than a 25% savings rate on $80,000 income.

Mistake 2: Ignoring Quality of Life

Extreme savings rates that make you miserable aren't sustainable. Find the highest rate you can maintain long-term.

Mistake 3: Not Adjusting for Life Changes

Your optimal savings rate changes with:

- Income level

- Family situation

- Age and health

- Career stability

Mistake 4: Comparing to Others

Your optimal savings rate depends on your goals, timeline, and circumstances. A 25% rate might be perfect for your situation even if someone else saves 50%.

Financial Wellness: Beyond Budgeting to Freedom

Most financial wellness programs focus on budgeting and expense tracking, but they miss a crucial dimension: freedom. True financial wellness isn't just about spending less — it's about designing a life where money supports your autonomy rather than constraining it.

The key insight is shifting from a scarcity mindset ("How do I cut costs?") to an abundance mindset ("How do I build systems that create time and optionality?"). This means prioritizing income security, expense optimization, system resilience, and time freedom as interconnected goals rather than isolated tactics.

For example, reducing your required income through lifestyle design can be more powerful than earning more, because every dollar you don't need is a dollar of freedom. Similarly, building location-independent income streams and anti-fragile financial systems protects you against single points of failure.

When evaluating your financial wellness, consider both primary metrics (savings rate, emergency fund months, investment income coverage) and secondary metrics (career optionality, geographic flexibility, time autonomy). The strongest financial position combines a high savings rate with systems that make you resilient to change — not just a bigger bank balance.

Why Traditional Financial Wellness Programs Fail

Most financial wellness programs focus narrowly on budgeting and expense tracking, which often creates a sense of restriction rather than empowerment. They treat money as a problem to be managed rather than a tool for building freedom. When your entire financial identity revolves around cutting costs, you miss the bigger picture: true financial wellness comes from aligning your money with your values and designing a life where work becomes optional. The key is shifting from a scarcity mindset to an abundance mindset—using your savings rate not as a measure of deprivation, but as a metric of optionality.

The Four Pillars of True Financial Wellness

Beyond budgeting, sustainable financial wellness rests on four interconnected pillars:

1. Reduce Your Required Income The lower your fixed expenses, the less you need to earn to maintain your lifestyle. This directly amplifies your savings rate and shortens your path to financial independence. Focus on optimizing housing, transportation, and food—the "big three" that typically consume 60-70% of most budgets.

2. Build Location Independence Geographic flexibility creates powerful arbitrage opportunities. Whether it's moving to a lower-cost area domestically or leveraging international living costs, location independence can slash your required income without sacrificing quality of life.

3. Create Time-Wealth Instead of Money-Wealth A high savings rate buys you time—the most non-renewable resource. The goal isn't just accumulating money; it's accumulating control over your calendar. Every percentage point increase in savings rate translates directly to years of freedom recovered.

4. Develop Anti-Fragile Financial Systems Build systems that strengthen under stress. This means diversified income streams, robust emergency funds, and investment strategies that don't require constant monitoring. Your financial plan should work even when life doesn't go according to plan.

Location Independence: A Hidden Lever of Financial Wellness

One of the most overlooked dimensions of financial wellness is the freedom to earn and spend in places that match your goals. Location independence means designing your income and lifestyle so you are not tied to a high-cost city or a single employer. For some, this looks like remote work from a lower-cost region; for others, it means building portable skills or income streams that travel with you. The result is the same: you reduce the income you need to fund a life you actually want, which directly raises your savings rate without forcing stricter budgeting.

Anti-Fragile Financial Systems

A savings rate alone won't protect you from black-swan events. Building anti-fragile financial systems means designing your money so that unexpected stress makes you stronger, not weaker. Start by diversifying income streams—no single employer or client should represent more than half your cash flow. Maintain a cash buffer beyond the standard emergency fund, and hold assets that perform differently under various economic conditions. The goal is to move from fragile (one paycheck away from crisis) to resilient (can weather shocks) to anti-fragile (opportunities emerge during downturns).

Measuring True Financial Wellness

While your savings rate is a powerful headline metric, true financial wellness requires a broader dashboard:

Primary Metrics:

- Savings rate (target: 30%+ for accelerated FI)

- Months of expenses covered by liquid assets

- Passive income as percentage of total expenses

Secondary Metrics:

- Income diversification score (how many independent sources?)

- Expense flexibility ratio (what percentage of spending is discretionary?)

- Time freedom index (hours per week you control entirely)

Tracking these alongside your savings rate gives you a complete picture of financial health—not just how much you're saving, but how resilient and flexible your financial life has become.

Primary and Secondary Financial Wellness Metrics

To know if you are truly making progress, separate your headline numbers from your supporting signals. Primary metrics include your savings rate, net worth trajectory, and the gap between your required income and your actual income. Secondary metrics track resilience: months of runway, the percentage of expenses covered by passive or semi-passive income, and the flexibility of your major cost categories. Watching both sets together prevents you from celebrating a high savings rate while ignoring a fragile income structure.

The Financial Wellness Assessment

Beyond tracking your savings rate, a structured financial wellness assessment helps you identify weak spots in your money system. Evaluate yourself across four dimensions: Income Security (how stable and diversified your earnings are), Expense Optimization (whether your spending aligns with your values), System Resilience (your ability to absorb shocks without derailing long-term goals), and Time Freedom (how much control you have over your schedule). Scoring each area on a simple 1–5 scale reveals where to focus next. Someone with a high savings rate but low time freedom, for example, may be financially efficient yet still far from true independence.

The Time Freedom Framework

Traditional financial wellness programs often focus on strict budgeting and deprivation, which is why many people abandon them. A more sustainable approach is the Time Freedom Framework, which shifts the focus from restriction to intentional design. Rather than asking "How little can I spend?", ask "How can I structure my finances so that my time belongs to me?"

The framework rests on four pillars:

- Reduce Your Required Income — Lower fixed obligations so you need less to live well. This creates optionality.

- Build Location Independence — Design income and lifestyle so you are not tied to a high-cost area.

- Create Time-Wealth Instead of Money-Wealth — Prioritize activities that generate freedom and fulfillment over pure accumulation.

- Develop Anti-Fragile Financial Systems — Build buffers and multiple income streams so setbacks strengthen rather than break your plan.

True financial wellness is not a score on a budgeting app. It is the degree to which your money supports the life you actually want to live.

Time-Wealth vs. Money-Wealth

Financial wellness is not just about the size of your portfolio; it is about who owns your calendar. Time-wealth is the ability to control how you spend your days, while money-wealth is simply the balance in your accounts. A high savings rate matters because it converts excess income into both: it grows your investments and reduces the future hours you must trade for money. As you optimize your savings rate, ask yourself whether each dollar saved is buying more money, more time, or ideally both.

Savings Rate by Life Stage

Early Career (20s)

- Target: 15-25%

- Focus: Build habits, increase income, avoid lifestyle inflation

- Priority: Emergency fund, then retirement accounts

Peak Earning (30s-40s)

- Target: 25-40%

- Focus: Maximize high-income years, optimize taxes

- Priority: Max retirement accounts, taxable investments

Pre-Retirement (50s+)

- Target: 30-50%

- Focus: Catch-up contributions, reduce risk

- Priority: Bridge accounts for early retirement

Want to track your savings rate and financial runway automatically? Check out our Financial Freedom Spreadsheet for a hands-on tool to monitor your progress and optimize your path to financial independence. You can also use a dedicated financial freedom tracker spreadsheet to visualize your FIRE number progress alongside your savings rate over time.

The Compound Effect of High Savings Rates

Here's why your savings rate matters more than investment returns:

Scenario A: Low Savings Rate, Great Returns

- 10% savings rate, 10% investment returns

- Timeline to FIRE: 46 years

Scenario B: High Savings Rate, Average Returns

- 40% savings rate, 6% investment returns

- Timeline to FIRE: 25 years

The high savings rate wins by over 20 years, even with significantly lower investment returns.

Why This Happens:

- You need less money to retire (lower expenses)

- You accumulate money faster (higher contributions)

- You have more money working for you sooner (compound growth)

Frequently Asked Questions About Savings Rate

What is a good savings rate?

A "good" savings rate depends on your goals. The traditional financial advice benchmark is 15-20%, which puts you on track for a standard 30-40 year retirement timeline. For early retirement (FIRE), you need 30-50%+. For context:

- 10-15%: Minimum for any meaningful wealth building

- 20-25%: Solid foundation—above average

- 30-40%: Aggressive wealth building; you'll have options in 20-25 years

- 50%+: FIRE fast track; financial independence within 10-17 years

Should I calculate savings rate on gross or net income?

Use gross income (pre-tax) for the most accurate FIRE planning. It captures your total economic output and makes comparisons across tax situations more meaningful. Net-income savings rates can inflate your apparent savings rate because you're dividing by a smaller denominator.

Do employer 401k matches count toward my savings rate?

Yes—absolutely. Your employer match is compensation you're converting directly into wealth. Excluding it understates your true savings rate. If you contribute 6% and your employer matches 3%, your true savings rate from that source is 9%.

What if I have debt? Does debt repayment count as savings?

Extra debt repayment counts if it's building net worth. Extra principal payments on a mortgage count because they build equity. Minimum required debt payments do not count—they're just maintaining your net worth baseline. High-interest debt (credit cards) should be eliminated before calculating a "true" savings rate, as the interest drag cancels out investment gains.

How does my savings rate affect my FIRE number?

Your savings rate affects your FIRE number in two ways:

- Higher savings = lower expenses = smaller FIRE number needed (you're proving you can live on less)

- Higher savings = faster accumulation = you hit your FIRE number sooner

This double effect is why each 5% improvement in savings rate shaves years—not months—off your timeline.

Can I reach financial independence with a low income?

Yes, but it requires a higher savings rate to compensate. Someone earning $40,000 with a 50% savings rate ($20,000/year invested) can reach independence in roughly 17 years. Someone earning $100,000 with a 15% rate ($15,000/year invested) takes longer. Income helps, but the rate is the engine. Explore your options with the emergency fund to freedom fund calculator.

Your Savings Rate Action Plan

Week 1: Calculate Your Current Rate

- Gather all income and expense data

- Calculate your true savings rate using the complete formula

- Determine your current FIRE timeline

- Set improvement targets

Comprehensive data management makes calculating and tracking your savings rate effortless

Comprehensive data management makes calculating and tracking your savings rate effortless

Week 2: Optimize the Big Three

- Analyze housing costs and alternatives

- Review transportation expenses

- Track food spending for one week

- Identify the biggest optimization opportunities

Week 3: Automate Everything

- Set up automatic transfers to investment accounts

- Increase 401k contributions

- Automate bill payments

- Create systems that make high savings rates effortless

Week 4: Plan Income Growth

- Research salary benchmarks in your field

- Identify skills that command higher pay

- Explore side income opportunities

- Set income growth targets for the next year

The Long-Term Perspective

Your savings rate isn't just about reaching FIRE—it's about creating options throughout your life:

- Career flexibility: High savings rates mean you can take risks, change directions, or weather industry downturns

- Family security: Financial cushions let you handle emergencies and support loved ones

- Life design: When money isn't a constraint, you can design your life around your values rather than financial necessity

The goal isn't to save as much as possible—it's to save enough to live the life you want, when you want to live it.

Tracking your savings rate monthly—alongside your net worth—is the most reliable way to stay on course. A net worth tracker spreadsheet paired with your savings rate gives you two complementary signals: how fast you're building wealth, and what the total looks like today.

What's your target savings rate, and what will it make possible in your life?

Savings Rate Calculator: Your Path to Financial Independence

Financial Planning:

- Financial Runway Calculator: How Long Can You Go Without Income?

- Financial Freedom vs Financial Independence: What I Wish I'd Known 10 Years Ago

- The Complete Guide to Planning (and Funding) Your Career Sabbatical

- Emergency Fund to Freedom Fund: Calculate Your Path to Financial Independence

FIRE Calculators:

- FIRE Number Calculator: What Is My FIRE Number?

- Coast FIRE Calculator: When Can You Stop Contributing?

- Lean FIRE Calculator: Minimize Expenses, Maximize Freedom

- Fat FIRE Calculator: Enjoy Life While Building Wealth

Tracking Your Progress:

- Expense Tracker Google Sheets Template: Complete Setup Guide (2025)

- Financial Freedom Tracker Spreadsheet: Monitor Your Path to Optional Work

- Net Worth Tracker Spreadsheet: Build Your Complete Financial Picture

- financial independence number calculator

- savings interest calculator uk

financial independence journey

Expertise: After reaching a net worth of $1.6 million by age 36 through consistent investing and expense tracking, I can tell you that understanding and maximizing my savings rate was the key driver of that success.

Try our free Investment Tracker to monitor your savings rate and track your progress to financial independence.

Frequently Asked Questions

What is a savings rate and why does it matter?▾

Your savings rate is the percentage of income you save and invest instead of spending. It directly determines how quickly you can reach financial independence and retire early.

How do I calculate my true savings rate?▾

Divide your total monthly wealth building—including 401k contributions, employer matches, IRA deposits, and extra savings—by your gross monthly income, then multiply by 100.

What is a good savings rate for financial independence?▾

A savings rate of 50% or higher is ideal for reaching financial independence within 15–20 years, while 20% is a common baseline that typically requires 35–40 years.

How can I increase my savings rate?▾

Track spending to find waste, automate transfers to investment accounts, maximize employer 401k matches, and avoid lifestyle inflation as your income grows.

Does my savings rate affect my FIRE timeline?▾

Yes. A higher savings rate dramatically shortens your path to FIRE because you are simultaneously saving more and needing less to sustain your lifestyle.

Automated investment tracking with broker imports

- Auto-import IBKR & other brokers

- Options P&L, LEAPS & income

- Free trial, no card required

Built for options and stock traders

Related Articles

Progressive Emergency Fund Strategy: 6 Months to

Why stopping at 6 months of emergency savings limits your potential, and how to build a progressive fund that creates real financial independence.

financial independenceFinancial Freedom Trust in NZ: Protect Assets & Cut Tax (2026 Guide)

Complete guide to using trusts for financial freedom in New Zealand. Learn how family trusts can protect assets, reduce taxes, and accelerate your path to independence.

financial independenceFinancial Independence Number Calculator | Free FI Tool

Your financial independence number is the invested portfolio size that lets you live on investment returns indefinitely. This guide shows you how to calculate it, what variables matter, and how to reach it faster.

Financial IndependenceSavings Interest Calculator UK: How Much Will You Earn?

A UK savings interest calculator shows you exactly how much interest your savings will earn—and how much tax you might owe. This guide explains how UK savings interest works, covers the Personal Savings Allowance, ISA limits, and walks through the calculation step by step.

Personal Finance Tracking