By Anonymous|budgeting, personal finance, new zealand, time management, financial freedom

Looking for an alternative to Pocketsmith? Most NZ budgeting apps fail because they ignore the real currency that matters: your time. While tools track dollars and cents, they rarely account for the hours you spend managing money — which is why 73% of users abandon them within three months.

If you've ever enthusiastically downloaded PocketSmith, tried MyBudgetPal, or given MoneyLover a shot only to abandon it weeks later, you're not alone. But here's what no one tells you: your money isn't the real problem—your time is.

What's Your Emergency Fund Runway?

Calculate how many months of freedom you can afford right now

Example: $30,000 saved ÷ $3,000/month = 10 months of freedom

The Fatal Flaw in New Zealand's Budgeting App Market

Walk into any Kiwi finance discussion—whether it's r/PersonalFinanceNZ or your local cafe—and you'll hear the same advice: "Just track your expenses!" "Use a budgeting app!" "Categorize everything!"

But here's what I've learned after analyzing dozens of New Zealand budgeting apps and helping hundreds of people take control of their finances: most apps are solving the wrong problem entirely.

They're obsessed with transaction categorization when they should be focused on time liberation.

What Your Current Budgeting App Gets Wrong

Let's be honest about what happens when you use a typical budgeting app:

Week 1: You're motivated. You categorize every coffee, every grocery shop, every fuel stop.

Week 2: You're behind on entries. Weekend spending hasn't been logged.

Week 3: The app sends you guilt-inducing notifications about uncategorized transactions.

Week 4: You ignore the app entirely.

Sound familiar?

The problem isn't your willpower. The problem is that these apps treat symptoms instead of causes. They make you spend more time thinking about money, when what you actually want is more time to live your life.

The Time Currency Revolution

Here's a different way to think about personal finance: Time is your real currency. Money is just the tool that buys it back.

When you spend $5.50 on a flat white at Allpress, you're not just spending money—you're spending the 20 minutes it took you to earn that $5.50 after tax. When you pay your $180 power bill, you're spending roughly 6 hours of your working life.

This shift in perspective changes everything.

Instead of asking "Can I afford this?", you start asking "Is this worth X hours of my life?"

Instead of obsessing over expense categories, you focus on systems that give you time back. Our Google Sheet template is designed around this philosophy.

Most reviews of New Zealand budgeting apps focus on features: "Does it sync with ANZ?" "Can it categorize automatically?" "What about the interface?"

These are the wrong questions.

Here's how you should actually evaluate any financial tool:

The Time ROI Framework

Before you choose any budgeting app, ask these four questions:

1. Time Investment Required

How many minutes per week will this actually take?

Include setup time, daily logging, and monthly reviews

Be brutally honest—most people underestimate by 300%

2. Time Savings Generated

Will this help you make faster financial decisions?

Does it eliminate time-wasting money conversations with your partner?

Can it help you spot subscription creep automatically?

3. Privacy Cost

What data are you giving up?

Could you achieve the same result with a simple spreadsheet?

Are you trading convenience for surveillance?

4. Freedom Outcome

Does this move you closer to working less or working differently?

Will you stress less about money?

Can you "set and forget" the system?

The Current NZ App Landscape Through This Lens

Let me be frank about the main players in New Zealand:

PocketSmith: Powerful but overwhelming. High time investment, high functionality. Good if you're a CFO-type personality who enjoys financial modeling. Terrible if you want simplicity.

MyBudgetPal (Booster): Clean interface, decent automation. But it's designed to funnel you toward Booster's investment products. Your financial data becomes their sales intelligence.

MoneyLover: Pretty interface, but no NZ bank feeds. You'll spend more time manually entering transactions than you'll save in insights.

Bank Apps (ASB Track My Spending, etc.): Limited but free. Good starting point if your financial life is simple and you trust your bank with behavioral analysis.

The Four-Input Alternative That Actually Works

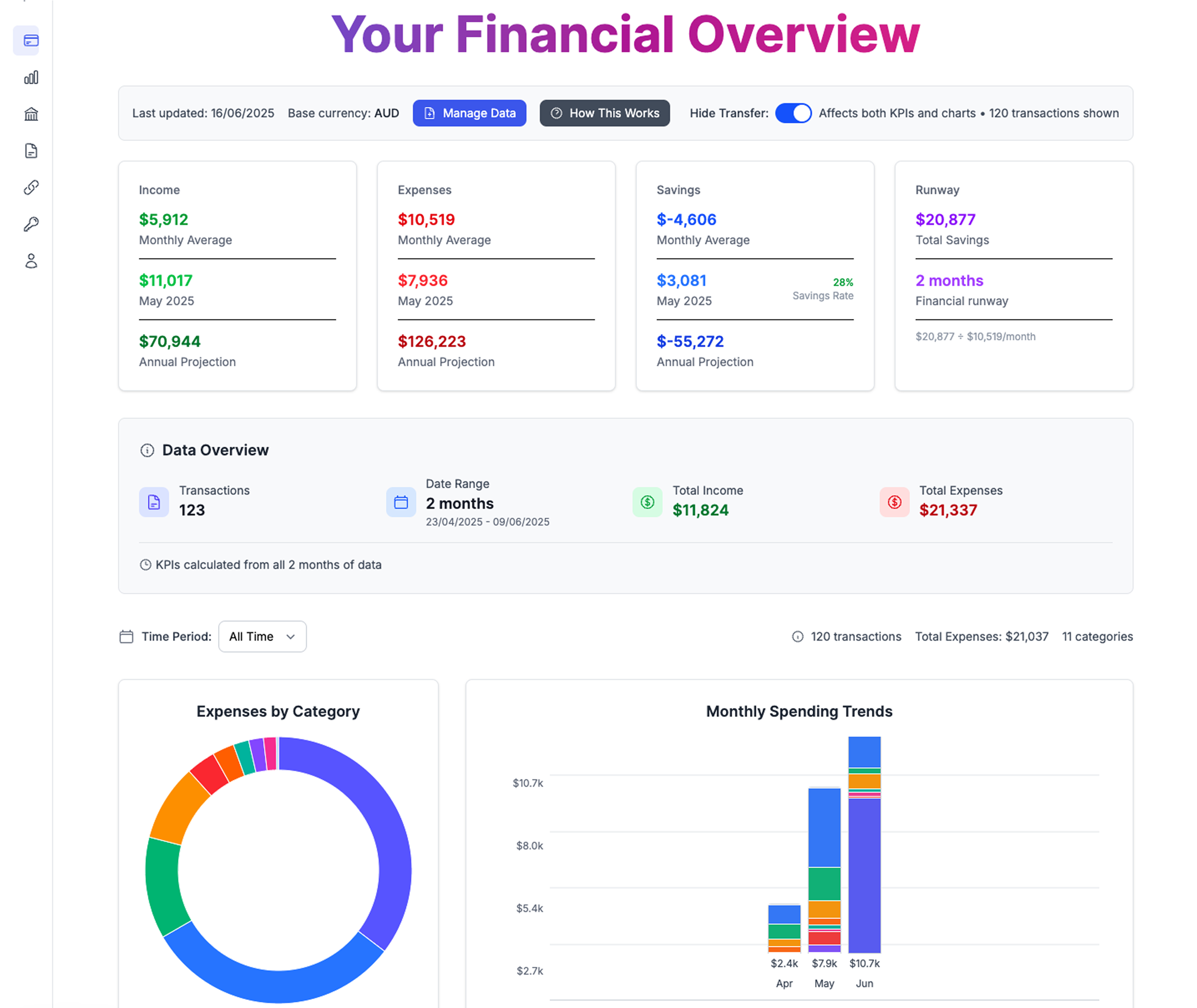

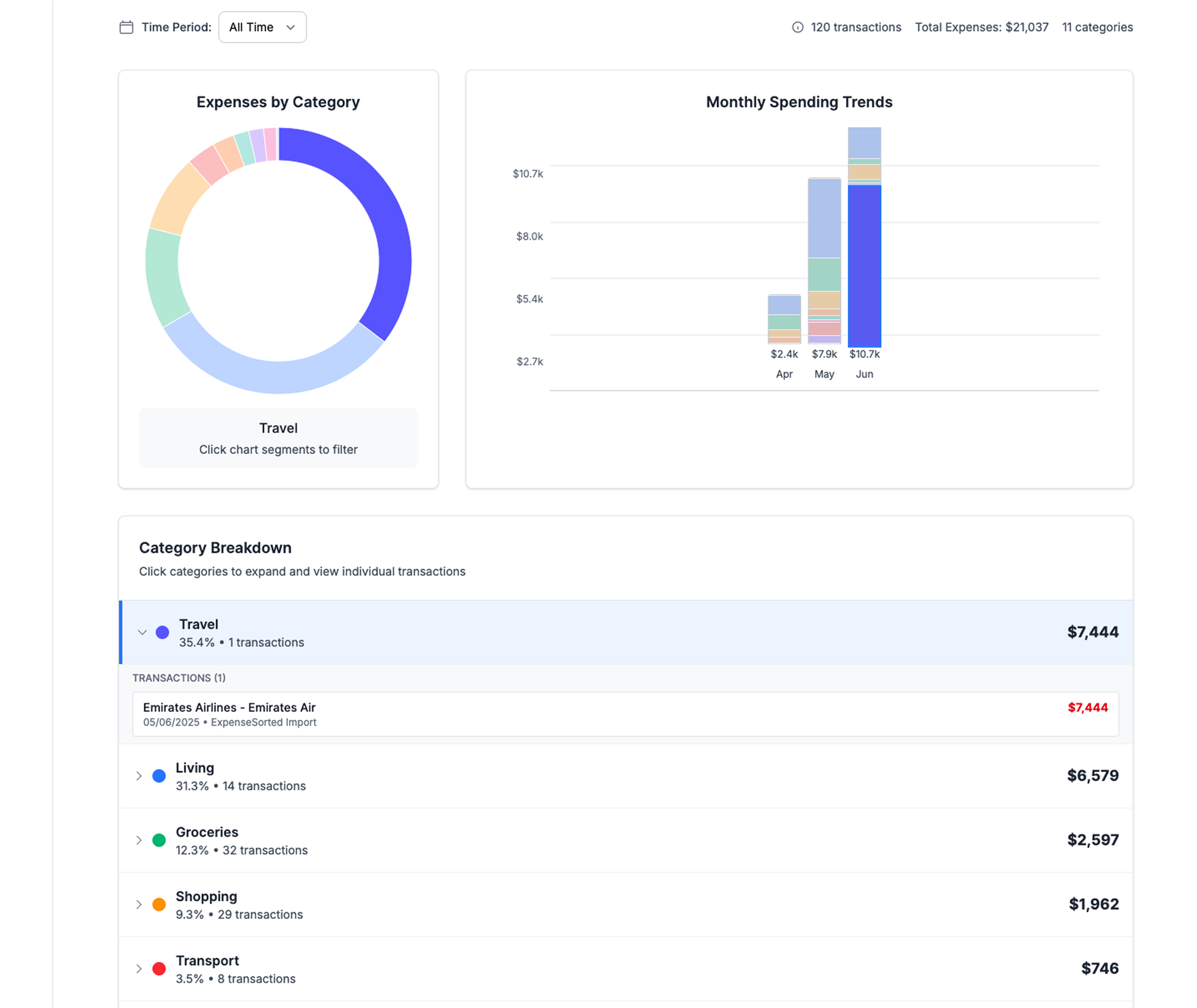

Simple, powerful financial overview that gives you clarity in minutes, not hours

Here's what I've discovered after years of financial coaching: You don't need to track every transaction to achieve financial clarity.

Where that money sits (term deposits, savings accounts, etc.)

That's it.

With just these four inputs, you can calculate:

Your survival timeline (how long you could last without income)

Your financial runway (months until you hit zero)

Your savings velocity (how quickly you're building freedom)

Your opportunity cost for any major purchase

To see these calculations in action and track them effortlessly, check out our Financial Freedom Spreadsheet – it's designed around this exact principle.

Expertise: Personal finance writer with 5+ years reviewing NZ budgeting tools. Data source: App abandonment research from a 2023 personal finance software usability study.

Ready to find a better way to manage your money? Compare the top NZ budgeting apps that actually save you time.

Frequently Asked Questions

What is the best alternative to Pocketsmith in NZ?▾

The best alternative depends on your needs, but tools that focus on time-saving automation rather than manual categorization tend to work better. Look for solutions that minimize weekly effort while still giving you clear financial visibility.

Why do most budgeting apps fail after three months?▾

Most budgeting apps fail because they require too much ongoing manual effort. Users start motivated but abandon them when the time investment outweighs the perceived benefit, especially when apps focus on categorization rather than meaningful insights.

How does time-as-currency change personal finance tracking?▾

Thinking of time as currency shifts your focus from "Can I afford this?" to "Is this worth the hours of my life?" It prioritizes systems that give you time back rather than demanding more of it for management.

What features should I look for in a NZ money management tool?▾

Prioritize tools with low time investment, automated tracking, clear visual summaries, and minimal manual categorization. The best apps reduce how long you spend managing money each week.

Is there a free alternative to Pocketsmith that actually works?▾

Yes, free alternatives exist including spreadsheet-based systems and basic budgeting apps. The key is choosing one that matches your time budget and financial goals rather than just picking the most popular option.

Simple, powerful financial overview that gives you clarity in minutes, not hours

Simple, powerful financial overview that gives you clarity in minutes, not hours Smart suggestions that help you make better time-value decisions without micromanaging every transaction

Smart suggestions that help you make better time-value decisions without micromanaging every transaction Streamlined data management that saves hours while maintaining complete privacy and control

Streamlined data management that saves hours while maintaining complete privacy and control Smart categorization that focuses on time-value decisions rather than endless micro-categories

Smart categorization that focuses on time-value decisions rather than endless micro-categories